How to translate your results into CFO's language?

Hello! I’m Caner, and welcome to my newsletter - SupplyChainist. Every Friday, I humbly write about subjects within supply chain management. By subscribing to the newsletter, you will get the weekly new edition to your inbox about the approaches that I discovered and keep learning to help you make smarter supply chain decisions.

Good Morning!

Last week, I wrote why the supply chain profession exceeded my expectations. I started in procurement and then transitioned to sales before becoming part of the supply chain team 5 years ago. Over the years, I started seeing supply chain decisions can actually increase shareholder value - which is C-suite’s target. That is why the supply chain function is powerful. In fact, we can (should) translate all our actions and performance to CFO’s language.

What is a shareholder value? The numerical answer is in the Balance Sheet.

Assets = Liabilities + Shareholder’s Equity.

One definition that explains the above equation well is a company has to pay all the things it owns (assets) by either borrowing money (liabilities) or taking it from investors (shareholder's equity).

If we can increase assets faster than liabilities, then shareholder’s equity will increase.

Total assets and liabilities are categorized as current (within 1 year) and non-current (+1 year horizon). If you are a mid-level supply chain manager, your decisions and performance will probably impact current assets and current liabilities. The non-current liabilities or non-current assets, which mostly would be fixed assets such as plant and property investments, are C-suite decisions. Therefore, we have the opportunity to increase the shareholder’s equity if current assets increase and current liabilities decrease. 1

As a supply chain professional, how can you impact current assets and current liabilities?

Total assets:

Current Assets

Cash and cash equivalents & Accounts Receivable (Goal is to increase)

Reduce order cycle time (Faster the order prepared and delivered, faster the payment)

Increase service levels (More product fulfilled, higher the invoice amount)

Improve invoice accuracy (More accurate invoices, faster the customer payment)

Inventories (Goal is to decrease. Remember inventory is not built up free of charge. As inventory increases, the accounts payable increases.)

Reduce average inventory levels (1- Work with vendors with shorter lead times and that don’t require high minimum order quantities, 2-Build forecasting and forecast error % review routine)

Other current assets (No supply chain impact)

Non-Current Assets

Other non-current assets, e.g. plants, properties, (C-suite decisions)

Total liabilities:

Current liabilities

Accounts Payable (Accrued payables - cash outflow)

Reduce vendor’s minimum order quantity requirements, which forces you to order more than you need.

Push out vendor payment terms (not preferred)

Other current liabilities (No supply chain impact)

Non-Current liabilities

Other long term debts (C-suite decisions)

Two other key liquidity metrics

There are two other metrics businesses track to measures a company's liquidity, operational efficiency, and short-term financial health.

1) Working Capital = Current Assets - Current Liabilities

If current assets > current liabilities, the company can at least pay its bills and continue to operate and continue to invest.

If current assets < current liabilities, the company can be in trouble.

Also measured as Current Ratio = Current Assets/Current Liabilities.

2) Cash Conversion Cycle = Days of Inventory Outstanding + Days of Sales Outstanding - Days of Payables Outstanding

It attempts to measure (in days) how long each net dollar input is held up in production, inventory, and sales before it gets converted into cash. 2

Days of Inventory Outstanding = Average Inventory/COGS

On average, how many days it takes to convert the inventory into sales.

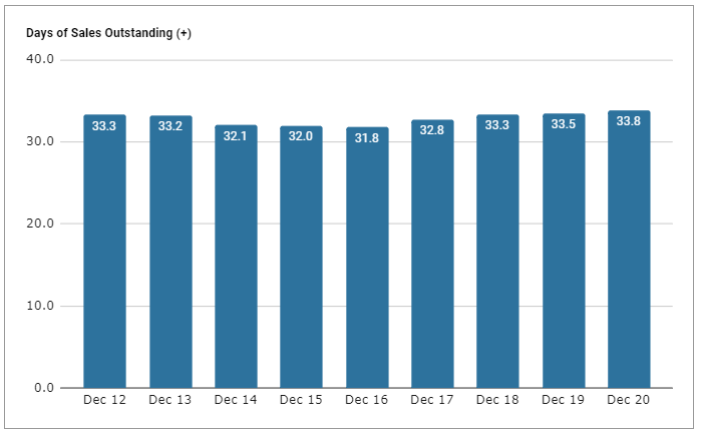

Days of Sales Outstanding = Average Accounts Receivable/Sales

On average, how many days it takes to get cash from customers.

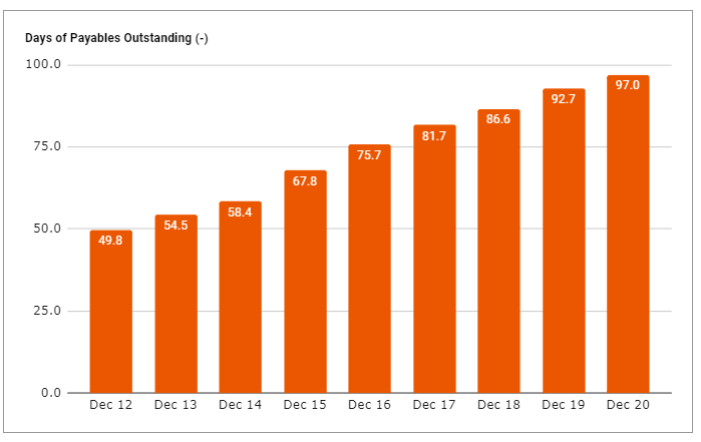

Days of Payable Outstanding = Average Accounts Payable/COGS

On average, how many days it takes to pay suppliers.

Check the balance sheet for inventory, accounts receivable, accounts payable, and income statement for sales and COGS.

Example - PepsiCo’s 10 years Cash Conversion Cycle

As of Dec 2020 statements, PepsiCo has a negative cash-conversion-cycle, which means they convert their inventory into sales and collect cash from customers 20 days before paying their vendors. A negative cash conversion cycle should help PepsiCo to increase its cash flow. In 2012, the situation was exactly the opposite; PepsiCo paid its vendors before getting paid by its customers.

So how could this have happened? Let’s remember the formula.

Cash Conversion Cycle = Days of Inventory Outstanding + Days of Sales Outstanding - Days of Payables Outstanding.

It takes PepsiCo, on average, 35-45 days to convert their inventory into sales. Over the past 4 years, it consistently increased, which wouldn’t help Cash Conversion Cycle to go negative.

PepsiCo collects cash from its customers in 30-35 days, which has been very consistent past 9 years.

On average, PepsiCo pays its vendors in 97 days. I would assume this was a critical goal for PepsiCo as the average consistently moved up every year. The increase in Payables Outstanding is the main reason why PepsiCo operates with a negative cash conversion cycle that should generate surplus cash for their business.

Want to see the full calculations? You have access to the SupplyChainist spreadsheet here: Cash Conversion Cycle Analysis

It is important to note that the cash-conversion-cycle metric applies to businesses that rely on inventory to generate revenue.

Can you now see the power of supply chain?

The best part?

For all the public companies, their financial statements are available online. If you understand these metrics, you could also see how your competitor or your industry is doing and where they focus.

Thank you for being part of SupplyChainist, and have a great Friday :)

If you liked this issue and found it valuable, consider sharing it with friends:

If you haven’t subscribed to it yet, subscribe now: